The alumina ceramics market, advancing from US$ 5.54 billion in 2025 toward US$ 7.75 billion by 2034 at a CAGR of 3.8% as per The Insight Partners, navigates genuine technical and commercial challenges that constrain adoption in applications where alumina would otherwise provide clear performance advantages over competing materials. The Alumina Ceramics Market Demand analysis from The Insight Partners identifies four primary barriers whose commercial consequences require specific examination.

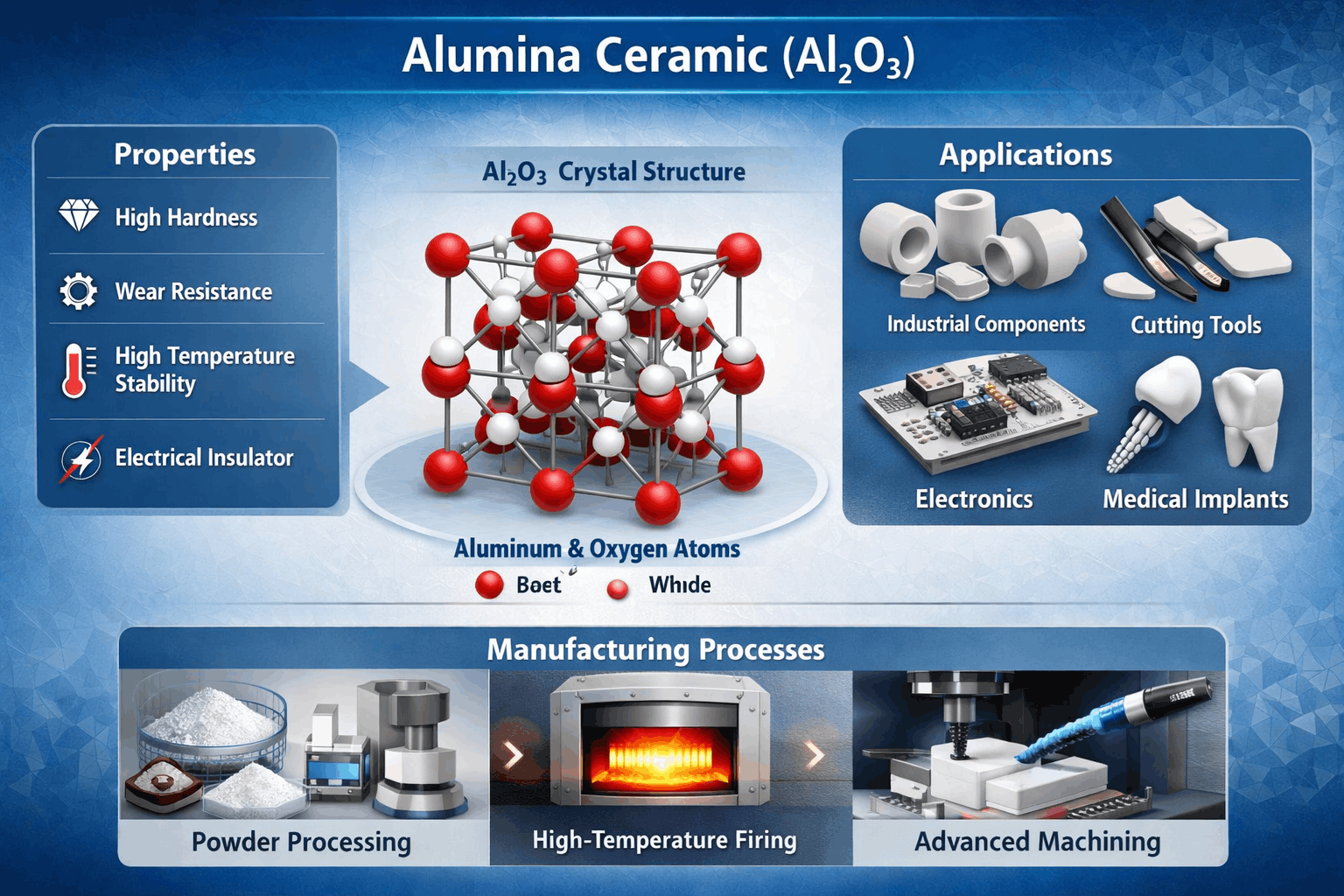

Brittle fracture is alumina ceramic's most fundamental application-limiting characteristic, representing a material behavior whose physical origins are inseparable from the same crystal chemistry that creates the hardness and thermal stability that make alumina commercially valuable. Crystalline aluminum oxide's strong directional ionic bonds resist plastic deformation that would redistribute stress concentrations in metals, instead concentrating stress at crack tips until fracture propagates catastrophically without the warning deformation that metal failure provides. This absence of plastic deformation means that alumina ceramic components can survive millions of service cycles under their design load before failing suddenly under a single impact or thermal shock event whose energy exceeds the fracture toughness threshold. Applications in dynamic loading environments including mechanical seals in pumping systems with vibration, wear plates in conveyor systems subject to lump impingement, and ballistic armor under repeated impact require careful engineering design to manage this fracture risk rather than treating it as simply a material property to specify around.

The precision machining cost of alumina ceramic components creates a manufacturing economics challenge that limits adoption in cost-sensitive applications despite clear performance advantages over metal alternatives. Alumina's extreme hardness that provides its wear resistance equally resists the metal cutting tools used in manufacturing, requiring diamond abrasive grinding operations whose specific material removal rate is orders of magnitude lower than metal cutting operations. This translates into machining time requirements that increase part cost substantially relative to equivalent metal component machining, creating economic break-even analyses where ceramic's extended service life must justify the premium initial acquisition cost over multiple component replacement cycles.

Check valuable insights in the Alumina Ceramics Market report. You can easily get a sample PDF of the report https://www.theinsightpartners.com/sample/TIPRE00019192

Key Market Players

- Saint Gobain S.A.

- Xiamen Innovacera Advanced Materials Co., Ltd.

- Ceramtec

- Sentro Tech

- LSP Industrial Ceramics, Inc.

- Morgan Advanced Materials

- Kyocera Corporation

- Dynamic Ceramic

- BMW Steels Ltd.

Thermal shock sensitivity limits alumina ceramic adoption in applications involving rapid temperature transitions that create differential thermal stresses exceeding the material's fracture toughness. Alumina's thermal conductivity, while higher than most engineering polymers, is significantly lower than metals, meaning that when one surface of a ceramic component is heated or cooled rapidly, the temperature gradient through the component thickness creates differential thermal expansion that manifests as tensile stress on the cooler surface. Refractory applications including kiln furniture and furnace components, and certain heat exchanger applications, face this thermal shock limitation that requires either design engineering mitigation through geometry optimization or acceptance of periodic replacement intervals that would not be required for metals with equivalent temperature service capability.

Supply chain concentration of high-purity alumina feedstock creates procurement vulnerability for ceramic manufacturers whose production quality is sensitive to aluminum oxide powder specification consistency. High-purity alumina powder meeting the chemical purity and particle size distribution requirements for advanced technical ceramics is produced by a limited number of specialty chemical manufacturers, creating supply concentration risk that became commercially visible during the pandemic-era supply chain disruption period when specialty raw material availability created production planning challenges across the advanced ceramics industry.

Frequently Asked Questions (FAQs)

Q1. What engineering design approach manages alumina ceramic's brittle fracture risk in dynamic loading applications?

Compressive pre-stress through shrink fit or interference fit assembly that places the ceramic component surface in compression rather than tension before service loading begins effectively postpones brittle fracture initiation by requiring the service tensile stress to overcome the compressive pre-stress before net tension develops at surface flaws, combined with fillet radius optimization at geometry transitions and load application area maximization to distribute contact stress, collectively enabling alumina ceramic service in dynamic applications where point loading or geometric stress concentrations without pre-stress management would create unacceptable fracture risk.

Q2. How is additive manufacturing of ceramic components addressing the precision machining cost challenge?

Ceramic additive manufacturing builds net-shape or near-net-shape components whose final geometry requires minimal post-print diamond grinding to achieve specification, dramatically reducing the material removal and machining time requirements compared to conventional production of machined components from oversize sintered blanks, making ceramic additive manufacturing economically competitive for complex geometries where conventional machining cost would otherwise price ceramic specification out of consideration versus metal alternatives.

About The Insight Partners

The Insight Partners is a one stop industry research provider of actionable solutions. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media and Telecommunications, Chemicals and Materials.

Contact Us

The Insight Partners

Phone: +1-646-491-9876

E-mail: sales@theinsightpartners.com

Also Available In: Korean | German | Japanese | French | Chinese | Italian | Spanish