Contact Center Software Market Overview

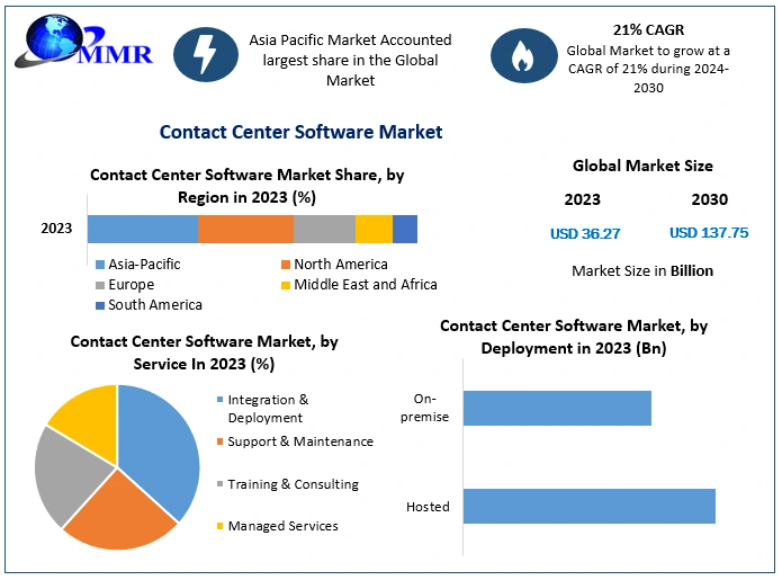

The Contact Center Software Market was valued at US$ 36.27 Bn in 2023 and is projected to grow at a CAGR of 21% from 2024 to 2030, reaching approximately US$ 137.75 Bn by 2030. Contact center software enables organizations to manage customer interactions across multiple communication channels, including voice, video, chat, email, mobile applications, and social media platforms, through a unified interface.

These solutions play a critical role in enhancing customer engagement, strengthening brand relationships, and improving operational efficiency. By automating and optimizing inbound and outbound communication workflows, contact center software allows enterprises to improve agent productivity, reduce response times, and gain actionable insights through real-time monitoring, analytics, and reporting. The growing emphasis on customer experience (CX), digital transformation, and omnichannel engagement continues to drive widespread adoption across industries.

To know the most attractive segments, click here for a free sample of the report:https://www.maximizemarketresearch.com/request-sample/6799/

Contact Center Software Market Scope

The scope of the Contact Center Software Market encompasses software platforms and associated services designed to streamline customer communication, workforce management, analytics, and service delivery. The market includes solutions deployed through on-premise, hosted, and cloud-based environments, catering to organizations of varying sizes and across diverse end-use industries.

This study evaluates market performance across key dimensions such as solutions, services, deployment models, enterprise size, end-user industries, and regions. The analysis also examines technological advancements such as artificial intelligence (AI), conversational analytics, virtual agents, and automation tools that are reshaping modern contact centers.

Research Methodology

The market analysis is based on a robust combination of primary and secondary research. Secondary research involved extensive review of industry publications, company annual reports, investor presentations, regulatory documents, and trusted databases. Primary research included interviews with key industry stakeholders such as software vendors, system integrators, CX managers, and technology consultants.

Market sizing and forecasting were conducted using bottom-up and top-down approaches, supported by data triangulation to ensure accuracy and consistency. Qualitative insights were incorporated to analyze market drivers, restraints, opportunities, and emerging trends, while quantitative models were used to estimate historical data and future projections from 2018 to 2030.

Market Segmentation Analysis

By Solution

The market is segmented into Automatic Call Distribution (ACD), Call Recording, Computer Telephony Integration (CTI), Customer Collaboration, Dialer, Interactive Voice Response (IVR), Reporting & Analytics, Workforce Optimization, and Others.

Among these, IVR solutions held the largest market share in 2023, driven by their ability to efficiently manage high call volumes, improve call routing accuracy, and enable self-service options. Meanwhile, customer collaboration solutions are expected to witness the fastest growth due to increasing demand for video- and image-based customer engagement.

By Service

Based on services, the market includes Integration & Deployment, Support & Maintenance, Training & Consulting, and Managed Services.

The integration & deployment segment dominated in 2023, supported by rising adoption of cloud-based platforms and the need to integrate contact center software with CRM and enterprise applications. The managed services segment is anticipated to grow at the highest CAGR, as organizations increasingly outsource IT operations to enhance scalability, performance, and cost efficiency.

By Deployment

Deployment models include On-premise and Hosted (Cloud-based) solutions.

On-premise deployments accounted for a significant revenue share in 2023 due to their customization and data control capabilities. However, cloud-based contact center solutions are gaining momentum owing to their flexibility, scalability, faster deployment, and enhanced analytics capabilities.

By Enterprise Size

The market serves Large Enterprises and Small & Medium Enterprises (SMEs). Large enterprises dominate adoption due to higher call volumes and complex CX requirements, while SMEs are increasingly adopting cloud-based solutions to improve customer engagement without heavy infrastructure investments.

By End User

Key end-use industries include BFSI, Consumer Goods & Retail, Government, Healthcare, IT & Telecom, Travel & Hospitality, and Others. The BFSI and IT & Telecom sectors remain major contributors due to high customer interaction intensity and compliance requirements.

To know the most attractive segments, click here for a free sample of the report:https://www.maximizemarketresearch.com/request-sample/6799/

Regional Insights

North America led the global Contact Center Software Market in 2023, accounting for more than 36% of total revenue. The region benefits from the presence of major market players, early adoption of advanced technologies such as AI and analytics, and strong demand from e-commerce, BFSI, and IT sectors.

Asia Pacific is expected to register the fastest growth during the forecast period, driven by the expanding ITES sector, rising digitalization among enterprises, and supportive government initiatives promoting cloud adoption and automation. Countries such as India, China, and ASEAN nations are witnessing increased investments in customer engagement technologies.

Europe continues to show steady growth supported by regulatory compliance requirements and increasing emphasis on customer experience optimization, while Middle East & Africa and South America are emerging markets driven by digital transformation initiatives and growing service industries.

Competitive Landscape and Key Players

The Contact Center Software Market is highly competitive, with key players focusing on product innovation, AI integration, strategic partnerships, acquisitions, and geographic expansion. Companies are increasingly investing in conversational AI, workforce optimization, and cloud-native platforms to strengthen their market position.

Key Market Players:

- 8X8, Inc. (US)

- Altivon (US)

- Amazon Web Services, Inc. (US)

- Amtelco (US)

- Aspect Software (US)

- Avaya Inc. (US)

- Avoxi (US)

- Cisco Systems, Inc. (US)

- Enghouse Interactive Inc. (US)

- Five9, Inc. (US)

- Genesys (US)

- Microsoft Corporation (US)

- Spok, Inc. (US)

- Talkdesk, Inc. (US)

- Twilio Inc. (US)

- UiPath (US)

- Unify Inc. (US)

- Exotel Techcom Pvt. Ltd. (India)

- Ameyo (India)

- ALE International (France)

- NEC Corporation (Japan)

- SAP SE (Germany)