Container Fleet Market: Driving Global Trade Through Innovation and Expansion

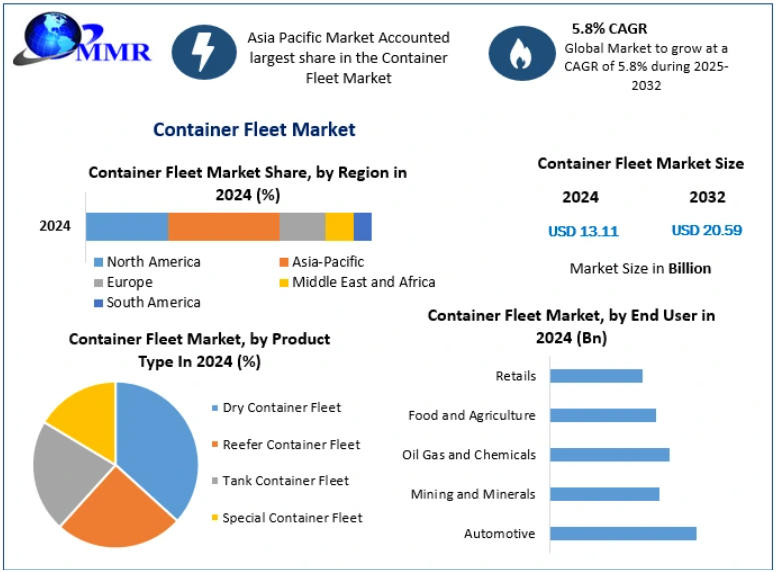

The global Container Fleet Market is a cornerstone of international commerce, valued at USD 13.11 billion in 2024 and projected to reach USD 20.59 billion by 2032, growing at a CAGR of 5.8%. Container fleets form the backbone of modern logistics, enabling standardized, cost-efficient transportation of goods across the globe. As international trade and e-commerce continue to expand, container fleets remain essential for businesses aiming to deliver products quickly, reliably, and sustainably.

Market Overview and Significance

Containerization has revolutionized global shipping by streamlining cargo transport and reducing logistical costs. This standardization allows for seamless handling of goods across ports, ships, railways, and trucks. The market encompasses diverse container types—including dry containers, reefer containers, tank containers, and specialized containers—serving industries ranging from automotive and chemicals to agriculture and retail.

The increasing globalization of trade, expansion of e-commerce, and demand for faster, traceable shipping solutions are key drivers of the container fleet market. Companies rely heavily on containerized shipping to maintain competitive supply chains and meet the expectations of a growing global customer base.

To know the most attractive segments, click here for a free sample of the report:https://www.maximizemarketresearch.com/request-sample/35879/

Market Dynamics and Trends

The container fleet industry is evolving rapidly, adopting digitalization, automation, and sustainability initiatives:

- Smart Containers & IoT Integration: Sensors and tracking systems enable real-time monitoring of cargo conditions, route optimization, and supply chain transparency.

- Sustainability: Shipping companies are investing in carbon-neutral vessels and eco-friendly operations to comply with International Maritime Organization (IMO) regulations and reduce environmental impact.

- Operational Efficiency: Companies are leveraging intermodal transportation solutions and advanced fleet management systems to maximize vessel utilization and reduce costs.

The market is influenced by fluctuations in freight rates and oversupply of vessels, creating challenges for profitability. However, strategic initiatives such as optimizing inventory, intermodal logistics, and operational efficiency are helping companies navigate these constraints.

Segment Analysis

By Product Type:

- Dry Containers: Represent the largest segment due to their versatility, cost-effectiveness, and ability to transport a wide variety of goods.

- Reefer Containers: Essential for temperature-sensitive goods, such as pharmaceuticals and perishable foods, ensuring quality and safety throughout transit.

- Tank Containers: Used for liquids and gases, particularly in chemical, petrochemical, and food industries, with robust safety features for hazardous cargo.

- Special Containers: Cater to niche logistics needs, including oversized or high-value cargo.

By End User:

Key industries relying on container fleets include automotive, mining and minerals, oil and gas, food and agriculture, and retail. Each sector benefits from efficient, reliable containerized shipping to support domestic and international supply chains.

To know the most attractive segments, click here for a free sample of the report:https://www.maximizemarketresearch.com/request-sample/35879/

Regional Insights

- Asia-Pacific: Dominates the market due to rapid industrialization, high export demand, and growing intermodal transportation infrastructure. China, Japan, and South Korea are central players in container manufacturing and fleet expansion.

- North America: The U.S. and Canada drive market growth with a robust industrial base, high import/export activity, and investments in advanced logistics infrastructure.

- Europe: Maintains a strong market presence with major shipping companies and extensive trade networks.

- Other Regions: Latin America, Middle East, and Africa show growing demand driven by trade expansion and logistics modernization.

Competitive Landscape

The container fleet market is highly competitive, featuring major shipping lines, leasing companies, and terminal operators. Key players include:

North America: Maersk Line (Denmark), Matson (USA), Hapag-Lloyd (Germany)

Europe: CMA CGM (France), Mediterranean Shipping Company (Switzerland), Westfal-Larsen (Norway)

Asia-Pacific: Kawasaki Kisen Kaisha (Japan), Evergreen Marine Corporation (Taiwan), COSCO Shipping (China), Hyundai Merchant Marine (South Korea), NYK Line (Japan), OOCL (Hong Kong)

These companies lead through fleet expansion, technological innovation, mergers and acquisitions, and sustainability initiatives, setting industry standards and driving global logistics trends.

Market Outlook

The container fleet market is poised for sustained growth, supported by:

- Increasing international trade volumes

- Rising e-commerce and consumer demand

- Technological innovation in smart containers and fleet management

- Environmental regulations prompting sustainable shipping solutions

As global commerce continues to expand and logistics networks become more sophisticated, container fleets will remain an indispensable component of the supply chain ecosystem, connecting industries and markets worldwide with efficiency, reliability, and scalability.