The global UV absorbers market is projected to witness strong expansion over the next decade, supported by tightening industrial specifications and rising polymer production across global manufacturing hubs. The market is expected to grow steadily, reaching approximately USD 1.1 billion by 2036, registering a CAGR of 5.3%, according to the latest analysis by Future Market Insights (FMI).

Market growth is being shaped by increasing application in plastics and coatings, growing consumer awareness regarding material degradation, and rapid adoption of advanced additive technologies. UV absorbers have evolved from specialized chemical additives into essential regulatory and quality requirements across automotive, packaging, and construction materials. While traditional benzophenones continue to dominate installations, manufacturers are increasingly integrating advanced systems such as hindered amine light stabilizers (HALS) and benzotriazoles to comply with modern durability expectations and improve weathering protection outcomes.

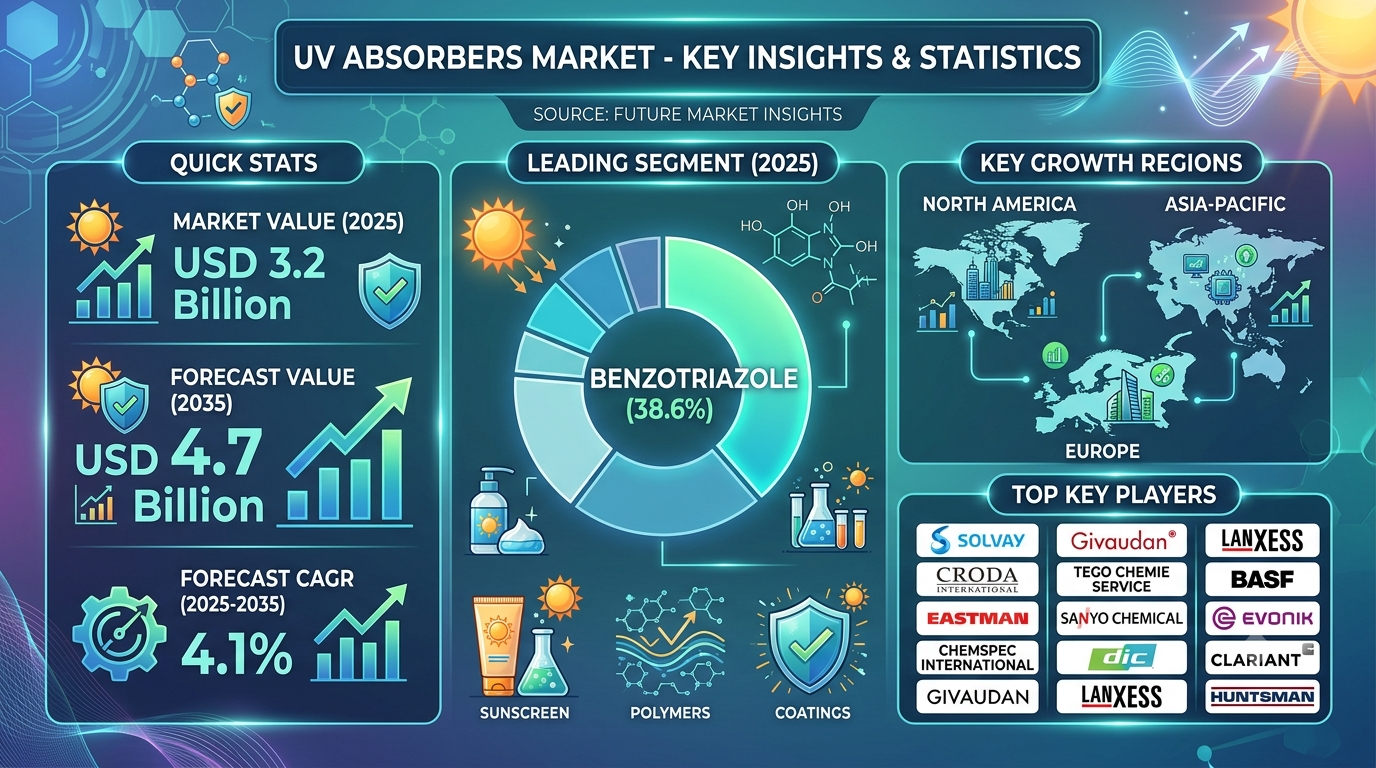

Global UV Absorbers Market Snapshot (2026–2036)

- Market size outlook toward 2036: USD 1.1 billion

- Forecast CAGR: 5.3%

- Dominant application category: Plastics and Polymers

- Fastest-growing segment: Water-borne coating formulations (~5.8% CAGR)

- Key growth regions: Asia Pacific, North America, Western Europe

- Primary demand channel: Direct industrial formulation integration

Momentum in the Market

Beginning from steady industrial adoption levels, the global UV absorbers market demonstrates accelerated growth throughout the forecast period as structural material longevity becomes mandatory across multiple countries. Between 2026 and 2036, expanding automobile manufacturing and rising infrastructure construction are expected to significantly boost demand for integrated light stabilizing systems.

Increasing urbanization and higher exposure to solar radiation are encouraging governments and material engineers to prioritize polymer protection technologies. From 2036 onward, innovation in high-molecular-weight chemical structures and integration with multi-functional additive masterbatches is expected to further strengthen market expansion. Smart stabilizers capable of adapting protection based on light intensity and temperature are emerging as key differentiators in new material formulations.

The Reasons Behind the Market’s Growth

Demand for UV absorbers is rising due to multiple structural and technological factors reshaping the global chemical ecosystem.

- Stringent Performance and Longevity Standards: Regulatory bodies are enforcing stricter structural lifetime warranties for exterior plastics and architectural elements, making UV light absorption a non-negotiable step in baseline formulation.

- Growing Polymer and Plastics Manufacturing: Rapid expansion of packaging production requires massive quantities of thin-film stabilizers to protect consumer goods from light degradation.

- Rising Industrial Coating Requirements: Commercial sectors are prioritizing advanced coating solutions that resist yellowing, chalking, and gloss reduction under continuous outdoor exposure.

- Eco-Friendly and Low-VOC Innovations: The rise of water-borne coatings is creating demand for redesigned, highly dispersible UV chemical absorbers tailored to modern environmental regulations.

Top Segment Application Type

Plastics and Polymers Lead Market Demand Plastics and polymers account for the majority of chemical installations across global markets, supported by increasing engineering plastic consumption and long-term infrastructure weathering needs requiring robust additive integration.

Chemical Type Analysis

- Benzotriazoles: ~4.9% CAGR driven by universal use in clear coatings and engineering resins.

- Benzophenones: ~4.5% CAGR supported by cost-effective applications in flexible packaging films.

- Triazines: ~5.6% CAGR with rising adoption in high-durability automotive topcoats.

- HALS combinations: ~5.8% CAGR, the fastest-growing synergistic stabilization segment.

Regional Development: Emerging Industrial Ecosystems Drive Expansion

Global manufacturing hubs are rapidly evolving their chemical processing networks, supported by localized production networks and highly efficient industrial supply chains.

- China and India: Regional volume manufacturing leaders and main chemical sourcing centers.

- United States & Germany: Advanced technological hubs expanding premium automotive and aerospace coating applications.

- South Korea & Japan: Specialization hubs scaling next-generation optical film and electronics stabilization.

Localized distribution partnerships between global chemical suppliers and regional plastic compounders are improving cost efficiency while accelerating localized product optimization.

Challenges, Trends, Opportunities, and Drivers

Drivers

- Mandatory material longevity specifications

- Rising global plastic manufacturing volumes

- Increasing infrastructure exposure protection needs

- Expansion of high-performance automotive clear coat demands

Opportunities

- Nanoparticle-based invisible UV screening technologies

- Biodegradable and naturally-derived stabilizing compounds

- High-temperature resistant masterbatches for engineering extrusion

- Integration with anti-oxidant multi-functional safety platforms

Trends

- Transition toward low-volatility, non-migrating additive systems

- Implementation of liquid chemical blends for automatic dosing systems

- Increased adoption of high-molecular-weight triazine chemistries

- Sustainability-focused synthesis paths reducing toxic waste by-products

Challenges

- Cost and pricing pressures for base commodities

- Strict migration limits in food-contact packaging regulations

- Technical challenges in dispersing solid powder additives into aqueous systems

Country Growth Outlook

The market’s growth trajectory is closely tied to industrial manufacturing rates and infrastructure deployment speeds across leading economies:

- China: Market volume leadership and continuous capacity additions.

- United States: Strict performance compliance adoption and automotive demand.

- Germany: High-end specialty chemical innovation and clear coat mastery.

- India: Rising demand for durable consumer electronics and construction plastics.

- Brazil: Increasing requirements for agricultural greenhouse film protection.

The Competitive Environment

The global UV absorbers market is moderately consolidated, with primary chemical providers competing through structural innovation, localized supply security, and rigorous regulatory certification. Leading companies include:

- BASF SE

- Songwon Industrial Co., Ltd.

- Clariant AG

- Solvay SA

- Adeka Corporation

These players are investing heavily in low-migration technologies, non-yellowing matrices, and environmental compliance systems while forming long-term distribution agreements with compounding networks to stabilize operational margins.

Future Outlook: Toward Resilient and Sustainable Materials

The global UV absorbers market is entering a transformative decade shaped by performance compliance, process optimization, and stricter chemical safety rules. Future stabilizer options are expected to function as combined material packages working smoothly alongside advanced heat stabilizers and specialized flame retardants. As manufacturing sectors mature and durability requirements strengthen, UV absorbers will remain central to achieving stronger and longer-lasting materials around the world.

Report Link: https://www.futuremarketinsights.com/reports/uv-absorbers-market