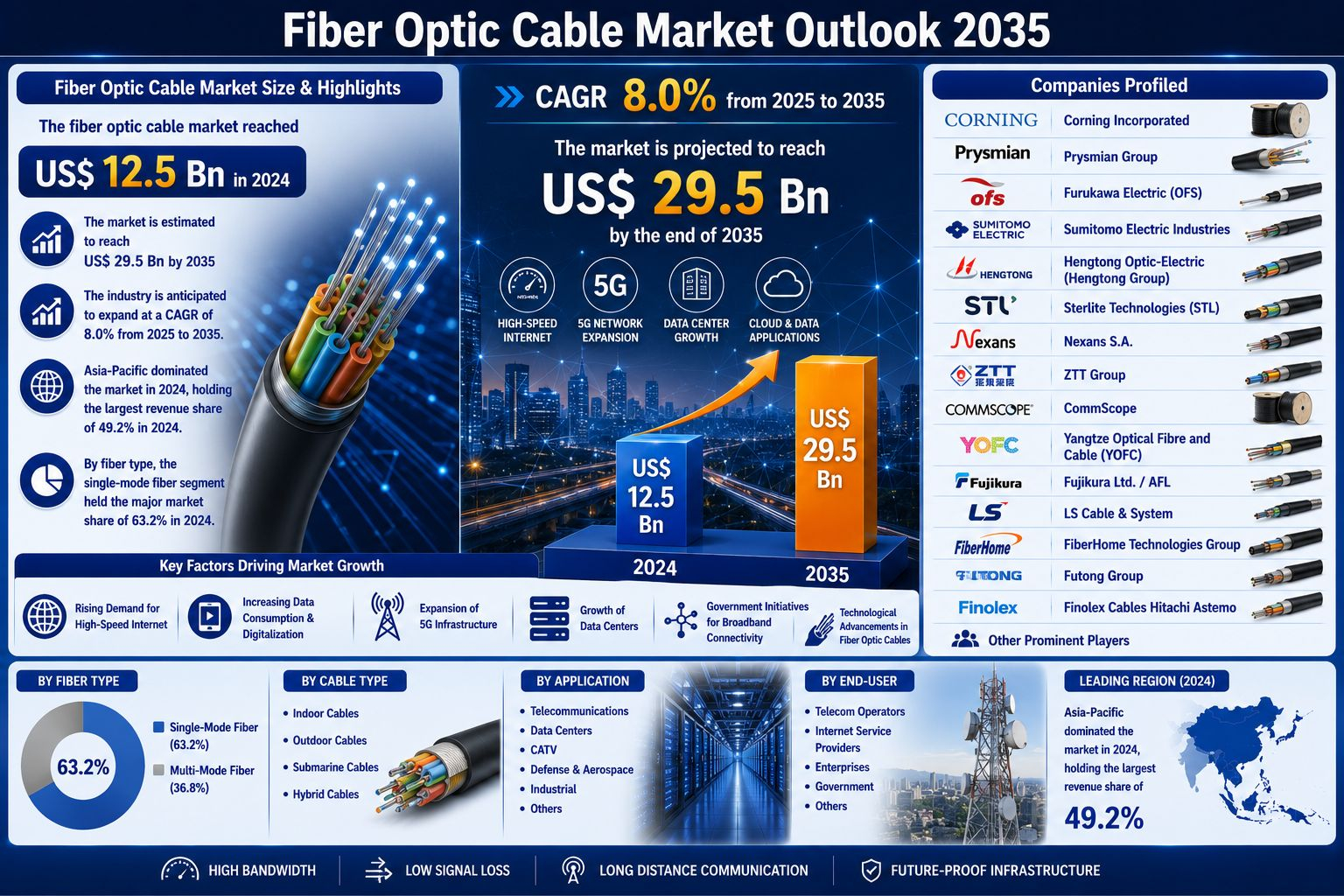

The global fiber optic cable market size was valued at US$ 12.5 Bn in 2024 and is projected to reach US$ 29.5 Bn by 2035, expanding at a CAGR of 8.0% from 2025 to 2035. The market is witnessing strong growth due to rising demand for high-speed internet, increasing deployment of 5G infrastructure, rapid expansion of cloud computing services, and growing investments in digital connectivity projects worldwide.

Analysts’ Viewpoint on Global Fiber Optic Cable Market

The fiber optic cable market continues to evolve rapidly as governments, telecom operators, cloud service providers, and enterprises invest heavily in digital infrastructure modernization. The growing need for ultra-fast internet connectivity, low-latency communication networks, and reliable data transmission systems is accelerating fiber optic cable deployment across multiple sectors.

The widespread adoption of cloud computing, artificial intelligence, Internet of Things (IoT), edge computing, video streaming platforms, and digital services has significantly increased global bandwidth requirements. As a result, telecom providers are replacing legacy copper networks with advanced fiber-optic infrastructure to support future communication demands.

Industry participants are focusing on product innovation, manufacturing expansion, and strategic partnerships to strengthen their competitive positions. Investments in bend-insensitive fibers, ultra-high-density cables, and next-generation fiber technologies are improving installation efficiency, reducing network deployment costs, and enhancing overall performance.

The continued rollout of 5G networks, smart city initiatives, hyperscale data centers, and rural broadband programs is expected to create substantial growth opportunities for fiber optic cable manufacturers over the forecast period.

Fiber Optic Cable Market Introduction

Fiber optic cables are transmission media that use light signals to carry data at extremely high speeds over long distances. Compared to conventional copper cables, fiber optics provide higher bandwidth, lower latency, greater reliability, and improved resistance to electromagnetic interference.

Fiber optic cables have become essential infrastructure components for telecommunications networks, broadband internet services, cloud computing environments, enterprise networks, healthcare systems, military communications, and industrial automation applications.

The increasing digital transformation of economies worldwide has accelerated the transition from traditional copper-based networks to fiber-based infrastructure. Governments and private organizations are investing significantly in broadband expansion projects to improve connectivity and bridge digital divides across urban and rural regions.

As demand for data-intensive applications continues to rise, fiber optic technology is expected to remain the foundation of next-generation communication networks.

Expansion of 5G Infrastructure Driving Market Growth

The rapid deployment of 5G infrastructure is one of the most significant drivers of the fiber optic cable market.

5G networks require ultra-low latency, high-speed, and highly reliable communication backhaul systems. Fiber optic cables provide the necessary connectivity between cell towers, small cells, base stations, and core network infrastructure.

Governments and telecom operators worldwide are investing billions of dollars to build fiber-rich networks capable of supporting advanced 5G services. The densification of cellular networks through deployment of small cells further increases demand for fiber connectivity.

The emergence of applications such as autonomous vehicles, industrial automation, augmented reality, virtual reality, and smart city infrastructure depends heavily on robust fiber networks that can support real-time data transmission.

Countries including China, India, the United States, Japan, and South Korea continue to accelerate 5G rollouts, creating significant demand for fiber optic cable installations throughout telecom infrastructure ecosystems.

As global 5G adoption expands, fiber optic cables will remain a critical enabling technology supporting network performance and scalability.

Rising Demand for Data Centers and Cloud Services Fueling Market Expansion

The rapid growth of cloud computing, artificial intelligence workloads, big data analytics, and digital services is generating unprecedented demand for high-capacity data transmission infrastructure.

Modern hyperscale and enterprise data centers require extensive fiber optic networks to support high-speed connectivity between servers, storage systems, cloud platforms, and edge computing facilities. Fiber cables provide the bandwidth and low latency necessary for maintaining optimal operational performance.

Organizations increasingly adopting hybrid cloud and multi-cloud environments require reliable interconnection solutions that enable seamless data movement across distributed infrastructures. Fiber optic technology serves as the backbone of these advanced networking environments.

Major cloud providers including Amazon Web Services (AWS), Microsoft Azure, and Google Cloud continue expanding global data center footprints to accommodate increasing demand for digital services. These investments directly contribute to higher consumption of fiber optic cables worldwide.

The growing importance of AI training clusters, machine learning applications, and real-time data processing further reinforces demand for advanced fiber optic infrastructure.

Market Opportunity: Expansion of Smart Cities and Broadband Connectivity Projects

The development of smart cities and national broadband programs presents significant opportunities for the fiber optic cable industry.

Governments around the world are investing heavily in digital infrastructure projects aimed at improving connectivity, enhancing public services, and supporting economic development. Fiber networks form the foundation of these initiatives by enabling reliable communication between devices, systems, and users.

Smart transportation systems, intelligent utilities, connected healthcare platforms, surveillance networks, and digital government services all require high-speed fiber connectivity.

At the same time, rural broadband expansion programs are creating new opportunities for fiber deployment in underserved regions. Public-private partnerships are increasingly supporting large-scale fiber installations to improve internet access and reduce digital inequality.

As nations continue prioritizing digital transformation strategies, demand for fiber optic cables is expected to rise substantially across both developed and emerging markets.

Single Mode Fiber Dominates the Market

Single Mode Fiber emerged as the dominant fiber type segment, accounting for approximately 63.2% of total market revenue in 2024.

The segment's leadership is primarily attributed to its superior performance in long-distance and high-bandwidth transmission applications. Single mode fiber minimizes signal attenuation and supports greater transmission distances compared to multi-mode alternatives.

Telecommunications operators, internet service providers, cloud infrastructure companies, and government agencies increasingly prefer single mode fiber for backbone networks, metro networks, long-haul communication systems, and submarine cable deployments.

The ongoing expansion of broadband infrastructure, 5G networks, and hyperscale data centers continues to strengthen demand for single mode fiber solutions worldwide.

As global data traffic volumes continue increasing, single mode fiber is expected to maintain its dominant market position throughout the forecast period.

Asia-Pacific Leads the Global Fiber Optic Cable Market

Asia-Pacific accounted for the largest share of the global fiber optic cable market in 2024, representing approximately 49.2% of total market revenue.

The region's dominance is driven by large-scale telecommunications investments, rapid urbanization, expanding internet penetration, and strong government support for digital infrastructure development.

China remains the largest producer and consumer of fiber optic cables globally. Massive investments in broadband networks, 5G deployment, smart cities, and industrial digitalization continue to support market growth across the country.

India is also witnessing significant expansion due to national initiatives such as Digital India, BharatNet, and ongoing fiber deployment projects aimed at connecting rural and semi-urban communities.

Japan and South Korea maintain advanced telecommunications infrastructures and continue investing in next-generation connectivity technologies, including 5G, IoT, and smart manufacturing systems.

Strong manufacturing capabilities, growing data center investments, and increasing demand for high-speed internet services position Asia-Pacific as the leading regional market for fiber optic cables.

Competitive Landscape

The fiber optic cable market remains highly competitive, with leading manufacturers focusing on capacity expansion, technological innovation, strategic partnerships, and product differentiation.

Companies are investing in advanced fiber designs, high-density cable architectures, and sustainable manufacturing practices to improve performance and reduce deployment costs.

Strategic collaborations with telecom operators, cloud service providers, governments, and infrastructure developers continue to strengthen market positions and expand global reach.

Key Players Operating in the Fiber Optic Cable Market

Major companies operating in the global fiber optic cable market include:

- Corning Incorporated

- Prysmian Group

- Furukawa Electric (OFS)

- Sumitomo Electric Industries

- Hengtong Optic-Electric (Hengtong Group)

- Sterlite Technologies (STL)

- Nexans S.A.

- ZTT Group

- CommScope

- Yangtze Optical Fibre and Cable (YOFC)

- Fujikura Ltd. / AFL

- LS Cable & System

- FiberHome Technologies Group

- Futong Group

- Finolex Cables

Recent Developments in Fiber Optic Cable Market

April 2025

Furukawa Electric unified its global optical fiber cable business under the new Lightera brand, aiming to strengthen innovation, operational efficiency, and global market presence in optical communication technologies.

July 2025

Fujikura Ltd. commenced commercial sales of the world's first 13,824-fiber SWR/WTC ultra-high-density fiber optic cable, designed to address increasing connectivity requirements of hyperscale data centers.

August 2024

Lumen Technologies signed a strategic agreement with Corning Incorporated to secure a long-term supply of next-generation fiber optic cables for large-scale network infrastructure deployments supporting data center growth.

July 2024

Sterlite Technologies (STL) introduced its advanced 864F Micro Cable, capable of accommodating 864 fibers within an 11.4 mm diameter cable using bend-insensitive HD A2 200-micron fiber technology.

Future Outlook

The global fiber optic cable market is poised for substantial growth through 2035, supported by accelerating digital transformation initiatives, widespread 5G deployment, increasing cloud computing adoption, and rising demand for high-speed internet connectivity.

Continuous investments in broadband infrastructure, hyperscale data centers, smart city projects, and next-generation communication networks will remain key growth catalysts. Manufacturers focusing on innovation, scalability, and high-performance fiber solutions are expected to benefit significantly from the expanding global demand for advanced optical communication infrastructure.