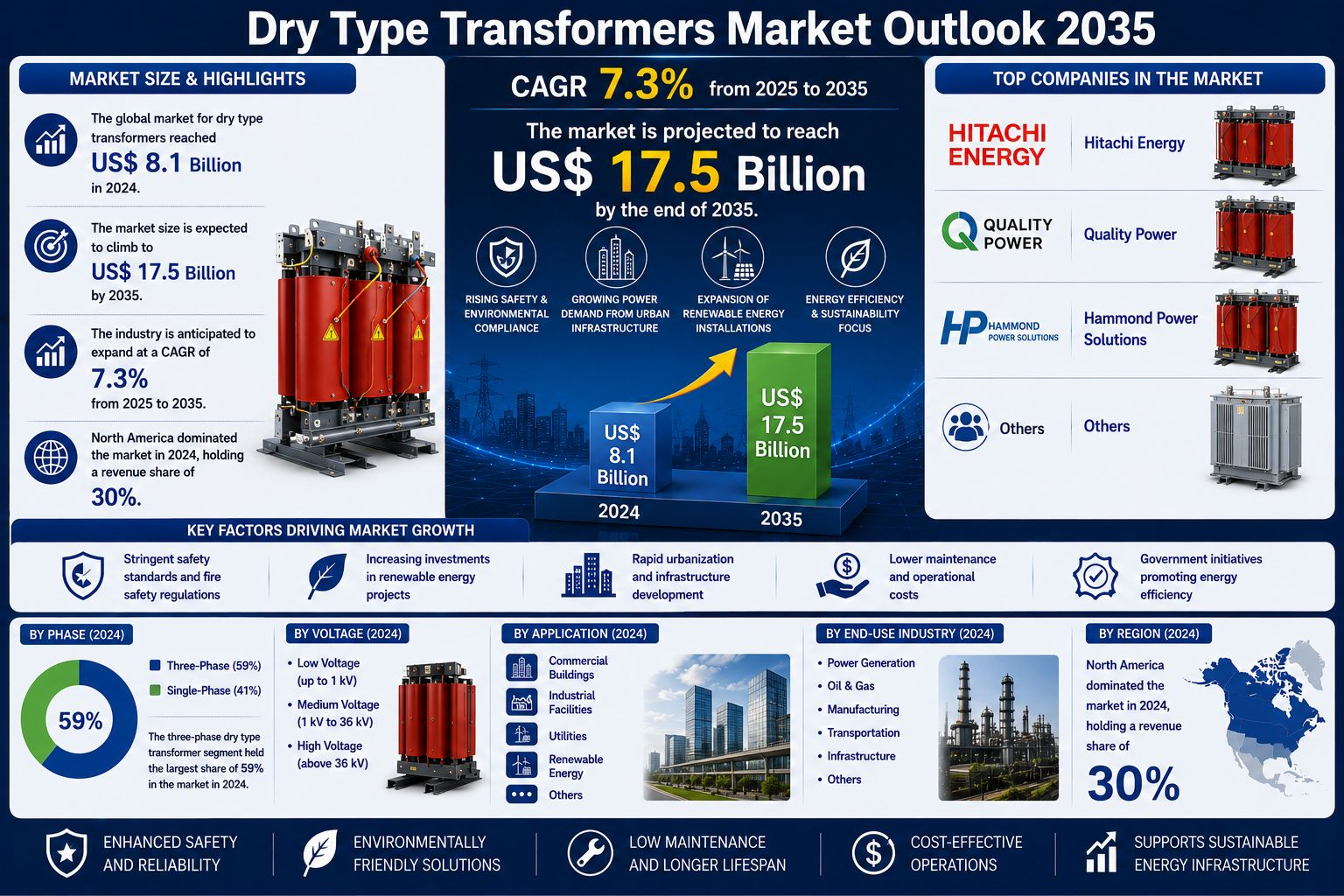

The global Dry Type Transformers Market was valued at US$ 8.1 Billion in 2024 and is projected to reach US$ 17.5 Billion by 2035, expanding at a compound annual growth rate (CAGR) of 7.3% from 2025 to 2035.

The market is witnessing significant growth as utilities, industrial facilities, commercial buildings, and renewable energy projects increasingly adopt dry type transformers to meet evolving safety, environmental, and energy-efficiency requirements. Rising investments in grid modernization, renewable power generation, urban infrastructure development, and mission-critical facilities such as data centers are further accelerating market expansion.

Unlike conventional oil-filled transformers, dry type transformers utilize air or solid insulation systems, eliminating the risks associated with oil leakage, fire hazards, and environmental contamination. As regulatory requirements become more stringent worldwide, organizations are increasingly transitioning toward safer and more sustainable transformer technologies.

Growing Safety and Environmental Regulations Driving Market Growth

One of the primary factors fueling growth in the global dry type transformers market is the increasing emphasis on safety and environmental compliance.

Traditional oil-filled transformers present potential risks related to oil leaks, fire incidents, and environmental contamination. As governments and regulatory bodies continue implementing stricter fire-safety standards and sustainability mandates, industries are actively seeking safer alternatives.

Dry type transformers offer several advantages, including:

- Oil-free operation

- Reduced fire risk

- Lower environmental impact

- Minimal maintenance requirements

- Enhanced operational safety

- Improved suitability for indoor installations

These benefits have made dry type transformers increasingly popular across hospitals, educational institutions, commercial buildings, airports, data centers, transportation networks, and industrial facilities where safety remains a critical priority.

Rising Urbanization and Infrastructure Investments Fueling Demand

Rapid urbanization and expanding infrastructure development worldwide are creating significant demand for advanced power distribution solutions.

Large-scale projects including smart cities, commercial complexes, metro rail systems, airports, manufacturing facilities, and mixed-use developments require reliable and efficient electrical distribution infrastructure.

Dry type transformers are particularly well-suited for such applications due to their compact design, low maintenance requirements, quiet operation, and ability to operate safely in confined indoor environments.

As urban populations continue to grow and governments invest heavily in infrastructure modernization, demand for dry type transformers is expected to remain strong throughout the forecast period.

Renewable Energy Expansion Creating New Growth Opportunities

The global transition toward renewable energy is emerging as a major growth catalyst for the dry type transformers industry.

Solar farms, wind power projects, battery energy storage systems (BESS), and hybrid renewable installations require highly reliable transformer technologies capable of managing fluctuating loads and variable operating conditions.

Dry type transformers offer several advantages for renewable energy applications:

- Superior thermal performance

- Enhanced resistance to environmental conditions

- Reduced maintenance requirements

- Improved harmonic handling capabilities

- Compatibility with inverter-based power systems

- Enhanced operational safety

Leading manufacturers are increasingly developing specialized dry type transformer solutions designed specifically for renewable energy integration and grid modernization initiatives.

Smart Monitoring and Digitalization Transforming Transformer Technologies

Digital transformation is reshaping the global transformer market as utilities and industrial operators increasingly adopt intelligent monitoring solutions.

Modern dry type transformers are being equipped with:

- Smart Sensors

- Real-Time Condition Monitoring

- Predictive Maintenance Systems

- IoT Connectivity

- Remote Diagnostics

- Asset Performance Analytics

These technologies enable operators to improve asset reliability, reduce downtime, optimize maintenance schedules, and extend equipment lifespan.

The growing adoption of smart grid infrastructure and digital substations is expected to further accelerate demand for digitally enabled dry type transformers.

Three-Phase Dry Type Transformers Lead the Market

Based on phase configuration, the Three-Phase Dry Type Transformer segment accounted for 59% of global market revenue in 2024, making it the largest segment within the industry.

The dominance of this segment is attributed to increasing demand from high-load applications including:

- Data Centers

- Manufacturing Facilities

- Commercial Buildings

- Metro Rail Networks

- Renewable Energy Projects

- Industrial Complexes

Compared to single-phase systems, three-phase transformers offer superior efficiency, improved voltage regulation, lower operating costs, and enhanced load balancing capabilities.

As industrialization and electrification initiatives continue expanding globally, demand for three-phase dry type transformers is expected to remain robust.

North America Maintains Market Leadership

North America accounted for approximately 30% of global Dry Type Transformers Market revenue in 2024, making it the leading regional market.

The region's dominance is driven by:

- Extensive grid modernization programs

- Expansion of hyperscale data centers

- Increasing renewable energy deployment

- Stringent environmental regulations

- Growing EV charging infrastructure

- Strong commercial construction activity

Utilities and commercial developers across the United States and Canada are increasingly adopting cast resin and vacuum pressure impregnated (VPI) transformers for critical infrastructure projects and indoor substation applications.

The growing focus on energy efficiency, safety compliance, and sustainability continues to strengthen North America's leadership position.

Asia Pacific Emerging as High-Growth Region

While North America currently leads the market, Asia Pacific is expected to witness substantial growth over the forecast period.

Rapid industrialization, urban development, expanding manufacturing sectors, and government-backed electrification initiatives are driving transformer demand across countries including:

- China

- India

- Japan

- South Korea

- ASEAN Nations

Investments in renewable energy infrastructure, smart grids, industrial parks, and commercial real estate developments are expected to create significant opportunities for dry type transformer manufacturers throughout the region.

Emerging Trends Shaping the Dry Type Transformers Industry

Several technological and market trends are transforming the future of the dry type transformers market:

- Cast Resin Transformer Adoption

- Smart Grid Integration

- Digital Monitoring Systems

- Predictive Maintenance Technologies

- Eco-Friendly Insulation Materials

- Renewable Energy Grid Integration

- Data Center Infrastructure Expansion

- Battery Energy Storage System Deployment

- IoT-Enabled Transformers

- Modular Substation Solutions

These developments are expected to improve operational performance while supporting long-term sustainability objectives.

Competitive Landscape

The global Dry Type Transformers Market is highly competitive, with leading manufacturers focusing on technological innovation, production expansion, strategic partnerships, and digital product development.

Major companies operating in the market include:

- Hitachi Energy

- Quality Power

- Hammond Power Solutions

- ABB

- Siemens

- Eaton

- GE Vernova

- Schneider Electric

- Crompton

- Kirloskar

- Hyosung

- Alfanar

- Elsewedy Electric

- MGM Transformers

- Virginia Transformer Corp.

- Rex Power Magnetics

- Voltamp Transformers Ltd.

- Acme Electric

- Bahra Electric

- Maddox Industrial Transformer, LLC.

Industry participants continue investing in cast resin transformer technologies, digital monitoring capabilities, and manufacturing capacity expansion to strengthen their market positions globally.

Recent Industry Developments

Several strategic developments highlight the industry's focus on innovation and capacity expansion:

- Hitachi Energy announced a €30 million investment to expand its dry type transformer manufacturing operations in Zaragoza, Spain, enhancing production capabilities and reducing lead times for European customers.

- In 2025, Hitachi Energy's HiDry 66/69 kV dry-type transformers were selected for a major offshore wind project in China, reinforcing the growing role of oil-free transformer technologies in renewable energy applications.

- Schneider Electric expanded its Trihal cast-resin transformer portfolio with IoT-enabled monitoring features and EcoStruxure Asset Advisor compatibility, supporting predictive maintenance and real-time asset visibility.

- Siemens Energy enhanced its GEAFOL cast-resin transformer portfolio with higher power density designs optimized for renewable energy, offshore, industrial, and urban applications.

These developments reflect the industry's ongoing commitment to sustainability, digitalization, and grid modernization.

Market Segmentation

By Product Type

- Cast Resin Dry-Type Transformer

- Vacuum Pressure Impregnated (VPI) Transformer

- Open-Wound Dry-Type Transformer

By Voltage Level

- ≤ 5 kVA

- 5 kVA to ≤ 30 MVA

-

30 MVA

By Phase

- Single Phase

- Three Phase

By Insulation Class

- Class A

- Class B

- Class F

- Class H

By Application

Industrial

- Chemical & Petrochemical Plants

- Oil & Gas Facilities

- Others

Commercial

- Buildings

- Hospitals

- Educational Institutions

- Shopping Malls

- Others

Residential

Utilities

- LV/MV Distribution Networks

- Battery Energy Storage Systems (BESS)

- Data Centers

- Others

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Market Outlook

The global Dry Type Transformers Market is positioned for strong growth through 2035 as utilities, industries, and commercial infrastructure operators increasingly prioritize safety, sustainability, and operational efficiency.

Rising investments in renewable energy projects, smart grids, urban infrastructure, electric vehicle charging networks, and hyperscale data centers are expected to create substantial demand for advanced transformer technologies.

As organizations continue transitioning toward environmentally responsible and digitally connected power distribution systems, dry type transformers are expected to play a central role in the future evolution of global electrical infrastructure.