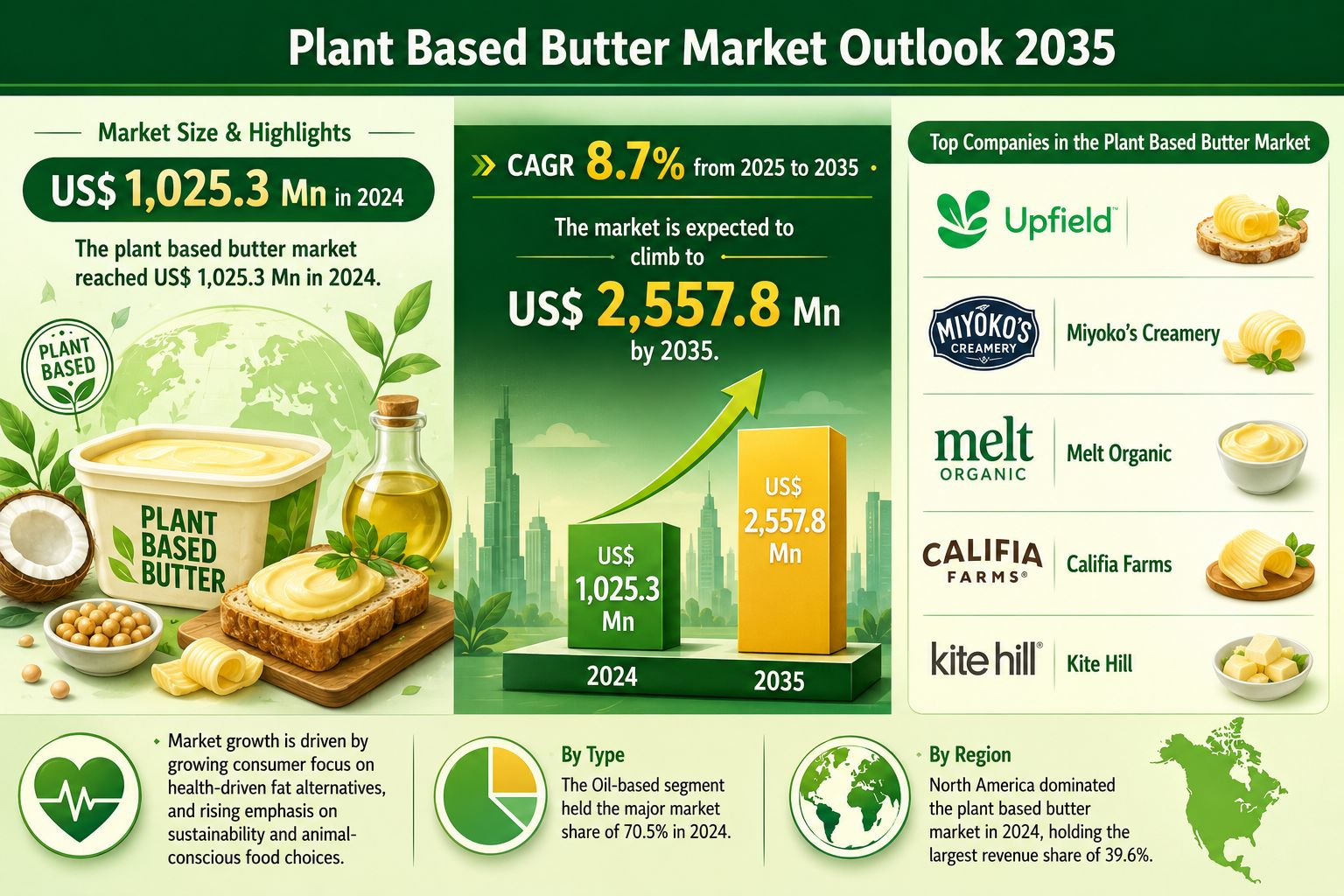

The global plant based butter market is witnessing significant growth as consumers increasingly seek healthier, environmentally responsible, and animal-friendly alternatives to traditional dairy products. Valued at US$ 1,025.3 million in 2024, the market is projected to reach US$ 2,557.8 million by 2035, expanding at a robust CAGR of 8.7% from 2025 to 2035.

The growing popularity of plant-forward diets, increasing awareness about cardiovascular health, and rising concerns regarding the environmental impact of livestock farming are creating favorable conditions for the expansion of the plant based butter industry. Manufacturers are responding by introducing innovative formulations that closely replicate the taste, texture, and cooking performance of conventional butter while offering improved nutritional profiles.

Growing Demand for Healthier Fat Alternatives Drives Market Growth

One of the primary factors fueling demand for plant based butter is the increasing consumer focus on healthier dietary choices. Public health discussions around cholesterol, saturated fats, and cardiovascular diseases have encouraged consumers to explore alternatives derived from plant oils and natural ingredients.

Unlike traditional dairy butter, many plant based butter products are formulated using oils such as olive, sunflower, canola, avocado, and coconut. These ingredients often contain higher levels of unsaturated fats and can be marketed as heart-friendly alternatives. Products enriched with omega-3 fatty acids and other functional ingredients are also gaining traction among health-conscious consumers.

The growing prevalence of cardiovascular diseases worldwide further strengthens the demand for healthier food products. According to global health organizations, cardiovascular diseases remain one of the leading causes of mortality worldwide, prompting healthcare professionals and nutrition experts to recommend diets that emphasize plant-based fats over animal-derived fats.

As a result, plant based butter is increasingly being viewed not only as a dairy substitute but also as a proactive dietary choice for maintaining long-term health and wellness.

Sustainability and Animal Welfare Trends Accelerate Adoption

Environmental sustainability has emerged as another major growth driver for the plant based butter market. Consumers are becoming more aware of the environmental impact associated with conventional livestock farming, including greenhouse gas emissions, water consumption, and land use.

Plant based butter manufacturers frequently position their products as environmentally friendly alternatives with lower carbon footprints than dairy butter. This message resonates strongly with environmentally conscious consumers, especially younger demographics who prioritize sustainability in their purchasing decisions.

Animal welfare concerns are also encouraging consumers to reduce their reliance on animal-derived products. The growing popularity of vegan, vegetarian, and flexitarian lifestyles has expanded the potential customer base for plant based butter products.

To strengthen sustainability claims, manufacturers are increasingly focusing on responsible sourcing practices, including the use of certified sustainable palm oil and traceable supply chains. Transparency in sourcing and production processes is becoming an important competitive advantage within the market.

Product Innovation Enhances Consumer Acceptance

The plant based butter category has evolved considerably over the past decade. Early products often struggled to match the flavor, texture, and performance of traditional butter. However, advances in food technology have enabled manufacturers to create products that deliver comparable results across a wide range of culinary applications.

Modern plant based butter products are designed to perform effectively in baking, cooking, sautéing, and spreading applications. Improved emulsification technologies and flavor development techniques have helped manufacturers achieve greater sensory parity with dairy butter.

The industry's future growth will depend heavily on continued innovation, pricing competitiveness, and supply chain efficiency. Companies are investing in clean-label formulations, improved fat blends, and enhanced product functionality to appeal to a broader consumer audience beyond vegans and lactose-intolerant individuals.

Oil-Based Products Dominate Market Segmentation

Based on type, the oil-based segment accounted for the largest share of the global plant based butter market in 2024, representing 70.5% of total revenue.

Oil-based products remain the preferred choice among manufacturers due to their scalability, cost efficiency, and ability to closely mimic the texture and melting characteristics of traditional butter. Common ingredients include blends of sunflower, canola, coconut, olive, and avocado oils.

The widespread availability of vegetable oil supply chains and the flexibility to adjust nutritional profiles have further contributed to the dominance of this segment. Manufacturers can formulate products with varying levels of saturated and unsaturated fats while maintaining desirable cooking performance.

Although oil-based products currently dominate the market, nut-based, seed-based, and oat-based alternatives are expected to gain popularity among consumers seeking premium, allergen-conscious, and specialty options.

North America Leads Global Market

North America emerged as the largest regional market in 2024, accounting for 39.6% of global revenue.

The region benefits from strong consumer awareness, high penetration of plant-based dairy alternatives, and widespread availability of vegan products across retail and foodservice channels. The United States and Canada continue to serve as innovation hubs for plant-based food development, with numerous brands introducing new products and formulations.

Retailers across North America are expanding their plant-based offerings, while restaurants and foodservice operators are increasingly incorporating vegan ingredients into their menus. These factors are expected to support continued market leadership throughout the forecast period.

Meanwhile, Europe remains an important market due to strong sustainability initiatives and established plant-based food cultures. Asia Pacific is expected to emerge as a high-growth region as urbanization, health awareness, and disposable incomes continue to increase.

Competitive Landscape and Recent Developments

The global plant based butter market features a mix of established food companies and specialized plant-based brands. Key industry participants include Upfield, Miyoko's Creamery, Melt Organic, Califia Farms, Kite Hill, Bunge, Conagra Brands, Violife, Milkadamia, Naturli' Foods, and WayFare Foods.

Industry consolidation and product innovation continue to shape the competitive landscape. In November 2025, Melt Organic acquired Miyoko's Creamery, gaining access to the company's plant-based butter and cheese formulations. The acquisition highlights growing competition and strategic investment within the sector.

Additionally, in October 2025, Better than Butter introduced a coconut-based plant butter product in the United States featuring organic ingredients and multiple certifications, reflecting increasing demand for clean-label and specialty products.

Future Outlook

The outlook for the global plant based butter market remains highly positive. As consumers continue to prioritize health, sustainability, and ethical consumption, demand for high-quality dairy alternatives is expected to rise steadily.

Advancements in ingredient technology, improved product performance, expanding retail distribution, and growing mainstream acceptance will further strengthen market growth. With plant based butter transitioning from a niche category to a widely accepted household staple, the industry is poised for substantial expansion over the next decade, reaching an estimated value of US$ 2.56 billion by 2035.